Scaling AI Responsibly: The Ultimate Secure AI Adoption Guide for Philippine BFSI

Philippine banks and financial institutions are navigating a rapidly evolving landscape where secure AI banking is becoming critical to daytoday operations. Transaction volumes are rising, digital channels are now the primary point of customer engagement, and customers increasingly expect seamless, realtime experiences. To meet these demands, Philippine BFSI organizations are accelerating the adoption of AI across core functions—from fraud detection and KYC to customer support and credit decisioning.

At the same time, these organizations operate under strict regulatory oversight, must safeguard sensitive customer data, and remain accountable for financial integrity—where even minor operational or compliance lapses can have immediate consequences. As AI becomes embedded in decisionmaking processes, the challenge for BFSI leaders is no longer simply adopting AI, but ensuring it is implemented securely, responsibly, and with clear governance controls in place.

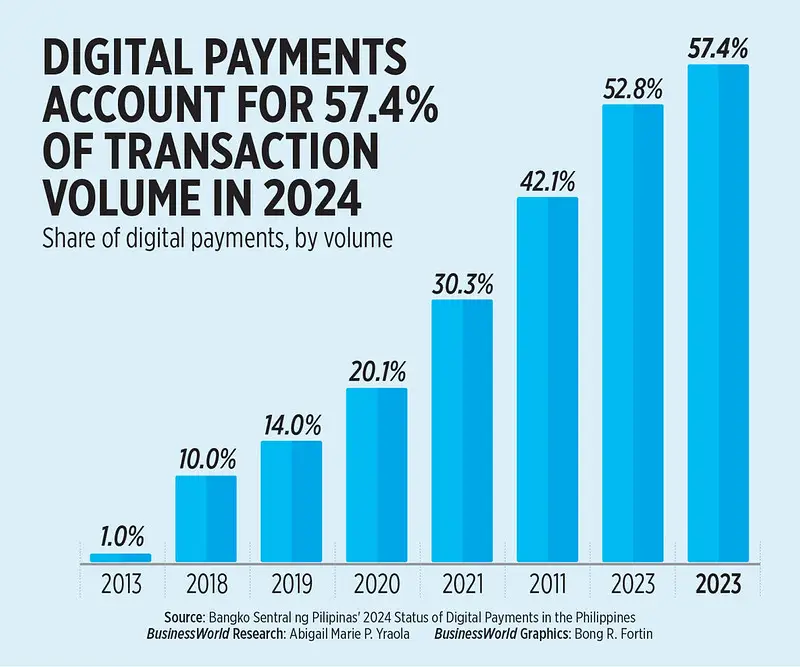

Digital financial activity in the Philippines has outpaced traditional in-branch transactions, reflecting widespread adoption of digital channels. According to the Bangko Sentral ng Pilipinas (BSP), digital payments accounted for 57.4% of total monthly retail transaction volume and 59% of transaction value in 2024, exceeding national digitalization targets and highlighting the shift from cash to digital finance.

This digital surge brings both opportunity and risk. Beyond operational efficiency, institutions face growing cybersecurity threats and complex fraud schemes. AI adoption not only helps process transactions faster but also strengthens real-time threat detection, anomaly monitoring, and predictive risk management.

Digital banks are heavily self-service, allowing customers to manage accounts through apps and websites. This surge in digital activity pressures banks to modernize operations and adopt technologies like AI to meet growing demand without compromising security, control, or compliance.

AI is now embedded in mission-critical processes from fraud detection and KYC reviews to credit decisions and real-time customer support. Each automated decision carries implications for operational performance, regulatory accountability, risk management, and cybersecurity posture.

Industry data shows that automation is concentrated in high-volume, repeatable, and compliance-sensitive operations. A 2025 Deloitte survey of Asia Pacific financial institutions, including Philippine banks, found that over 70% are automating or planning to automate KYC/identity verification, fraud monitoring, and customer service, while 58% are automating credit decisioning and risk analytics.

Similarly, a 2025 McKinsey report noted that up to 35% of risk and compliance activities, including suspicious activity monitoring, AML alert triage, sanctions screening, and regulatory reporting, can be automated using AI. Another benchmark study reported that over 60 % of institutions leverage AI to automate document processing, transaction monitoring, and exception handling.

For executives, the challenge is not whether AI can improve efficiency, but how to integrate it responsibly and securely. Embedding governance, oversight, and controls—including cybersecurity measures—ensures that AI supports business objectives without creating blind spots. Given these AI applications, it’s important to understand why the BFSI industry amplifies the need for secure adoption.

Why BFSI Is Different from Other Industries

Unlike most industries, Philippine banks and financial services organizations operate under direct regulatory supervision and are accountable for protecting customer funds, financial stability, and data integrity. As AI becomes embedded in core banking operations, this elevates AI adoption—and AI governance in financial services—from a technology consideration to a regulatory and governance priority.

In regulated BFSI environments, AI influences decisions that directly affect customer assets, financial integrity, and systemic stability. As a result, AI initiatives must be governed with the same rigor applied to risk management, compliance, and internal controls, rather than treated as standalone innovation programs.

And BFSI organizations must navigate several distinct responsibilities and risk considerations, including:

- Strict regulatory oversight

The Bangko Sentral ng Pilipinas (BSP) requires that all systems supporting operations and decision-making, including AI-assisted processes, meet standards for governance, risk management, and internal controls. These requirements exist because financial systems directly impact customer assets, market confidence, and systemic stability. Because of this, financial organizations must maintain full visibility into where AI is used, define clear ownership of AI-supported decisions, and ensure that outcomes are consistent, explainable, and auditable. AI cannot be treated as a standalone tool—every application must be governed and defensible under regulatory review.

- Data privacy obligations

The Data Privacy Act of 2012, enforced by the National Privacy Commission (NPC), requires organizations to protect personal and sensitive financial data throughout its lifecycle. This exists because misuse or exposure of financial data can result in direct customer harm, legal liability, and loss of trust. Banks must control access to AI data, restrict the use of sensitive information, and ensure that AI activities comply with established data protection rules. AI systems handling sensitive data must incorporate encryption, access monitoring, and secure processing protocols to prevent unauthorized exposure.

- Growing cybersecurity and financial crime risks

BSP requirements on operational risk management and cybersecurity require financial organizations to detect, respond to, and manage threats that could disrupt services or compromise data. These expectations exist because cyber incidents and financial crime can directly affect customer funds, service continuity, and financial stability. Organizations must ensure AI-driven detection produces reliable alerts and supports timely response. Clear accountability structures are essential to prevent gaps that could escalate into regulatory and financial consequences.

These realities raise the bar for AI adoption in the Philippine BFSI. The challenge is no longer whether AI can improve speed or efficiency. It is whether organizations can scale it without weakening governance, increasing exposure, or losing control over regulated operations.

What’s Stopping BSFI from Adopting AI

Adopting AI in the Philippine BFSI is a transformation that interacts with governance, organizational behavior, and external pressures. Challenges emerge both internally and externally, and they can affect compliance, operational resilience, and customer trust if left unaddressed.

Internal Challenges

- Fragmented Adoption Across Departments

In many BFSI organizations, AI efforts often start in different departments — like operations, customer service, risk, or compliance — without a shared direction. The pain point is that teams end up using AI in different ways, with different rules and priorities, making it hard to scale, govern, and ensure the business moves in a single, secure, and strategic direction.

- Decision Accountability and Traceability

As AI becomes part of decisions like transaction approvals, fraud checks, or risk assessments, the pain point is that it can become unclear who is accountable when a decision is wrong—and whether the organization can clearly explain how that decision was made in the first place.

- Integrating AI Into Existing Risk and Compliance Frameworks

BFSI institutions operate under established risk, audit, and compliance protocols. The pain point is that AI often introduces processes that don’t fit neatly into these frameworks, making it difficult to monitor, validate, and report AI-driven activities consistently. This can lead to oversight gaps, regulatory challenges, and increased operational risk.

External Challenges

- Regulatory Expectations for Novel AI Use Cases

Regulators expect BFSI firms to ensure all decision-making and operational processes are transparent, auditable, and defensible, even as AI introduces new methods or insights. The pain point is that emerging AI applications can create uncertainty around compliance, making it hard for BFSI organizations to demonstrate accountability, satisfy regulators, and avoid potential fines or corrective actions.

- Customer Trust and Perception

AI increasingly shapes customer-facing processes, from advisory interactions to risk-informed recommendations. The pain point is that errors, delays, or unclear AI outputs can quickly erode customer trust, lead to complaints, and damage the brand’s reputation—making it harder for BFSI organizations to maintain loyalty and confidence in their services.

- External Vendor and Technology Dependencies

Many BFSI organizations rely on third-party AI platforms, cloud solutions, or analytics providers. The pain point is that these external systems can introduce vulnerabilities—such as data breaches, service disruptions, or compliance gaps—that the organization may struggle to control, creating operational, regulatory, and reputational risks.

The priority is not to limit innovation, but to enable it in a way that aligns with regulatory expectations, protects sensitive data, and preserves trust. As organizations move from understanding these challenges to acting on them, the focus shifts to how AI can be adopted securely without introducing new risks.

For a practical perspective on this, explore How Can Banks Achieve Secure AI Adoption Without Compromising Compliance.

If There are Challenges, How Do Philippine BFSI Organizations Address AI Adoption?

As Philippine BFSI organizations move beyond experimentation, the focus is shifting from whether to adopt AI to how to adopt it responsibly. Addressing the challenges of AI adoption requires more than isolated fixes; it demands coordinated, organization-wide responses that align technology with governance, risk management, and operational realities.

Leading organizations are taking deliberate steps to close the gaps identified earlier:

- Moving from Fragmentation to Centralized Governance

Rather than allowing teams to deploy AI independently, organizations are establishing centralized governance structures that define standards, ownership, and accountability. This creates consistency in how AI is implemented, monitored, and evaluated across business units, reducing the risk of blind spots and inconsistent controls.

- Embedding Accountability into AI-Supported Decisions

To address unclear ownership, BFSI leaders are reinforcing human accountability alongside AI outputs. Decision ownership is clearly assigned, escalation paths are defined, and audit trails are maintained to ensure every AI-supported action can be traced, reviewed, and defended when needed.

- Integrating AI into Existing Risk and Compliance Frameworks

Instead of treating AI as a separate layer, organizations are embedding it directly into existing risk, audit, and compliance structures. This ensures that AI-driven processes follow the same controls, reporting standards, and validation requirements as traditional operations—closing gaps in oversight and ensuring regulatory alignment.

- Strengthening Customer-Facing Transparency and Control

To maintain trust, organizations are introducing clearer communication about AI-driven interactions and ensuring seamless escalation to human support when needed. This balances efficiency with reassurance, particularly in high-impact customer journeys like onboarding, transactions, and dispute resolution.

- Reinforcing Vendor and Technology Risk Management

As reliance on external platforms increases, BFSI organizations are tightening vendor governance—defining clear accountability for data protection, AI outputs, and service continuity. Continuous monitoring and stricter evaluation criteria help prevent third-party risks from becoming internal vulnerabilities.

These actions reflect a broader shift: AI adoption in BFSI is no longer just about capability; it is about control, accountability, and alignment with regulatory expectations. However, while these responses address individual challenges, they still require a unifying approach to ensure consistency and scalability across the organization.

Why Secure AI Adoption Is the Right Approach for BFSI

As organizations work to address the challenges of AI adoption, a clear pattern emerges: isolated solutions are not enough. Governance gaps, inconsistent controls, and fragmented implementations can persist without a cohesive, organizationwide strategy.

This is where secure AI banking, underpinned by strong AI governance in financial services, becomes critical. Rather than treating AI as a standalone innovation initiative, BFSI organizations must adopt a structured approach that embeds governance, accountability, and oversight into how AI is deployed and scaled.

Secure AI adoption in this context means enabling AI within clearly defined boundaries. It allows AI to scale across banking operations while maintaining visibility, control, and accountability at every stage of its use—ensuring that innovation does not come at the expense of regulatory compliance or customer trust.

For Philippine BFSI organizations, this approach directly addresses the core risks identified earlier:

- It reduces fragmentation by standardizing how AI is deployed and governed across teams

- It strengthens accountability by clearly defining ownership of AI-supported decisions

- It ensures regulatory alignment by embedding controls, auditability, and explainability into every use case

- It protects customer trust by maintaining transparency and safeguarding sensitive data

- It manages operational and vendor risk by enforcing consistent oversight across internal and external systems

More importantly, secure AI adoption creates a foundation for sustainable scale. Without it, AI initiatives may deliver short-term efficiency gains but introduce long-term risks that are harder to detect and control.

In a highly regulated environment like the Philippine BFSI, success is not defined by how quickly AI is adopted, but by how confidently it can be governed.

To understand how this approach translates into real-world impact, it is important to examine where AI is already being applied and how organizations balance efficiency with control in practice.

Where AI Is Making Practical Impact Today

As Philippine BFSI organizations shift from experimentation to AI-driven operations, the most meaningful impacts are emerging in areas where high volume intersects with compliance risk and customer expectations. These applications are not hypothetical — they reflect observable challenges and deployments in local financial organizations.

External-Facing Applications

- Chatbots and Virtual Assistants

Fragmented customer support and pressure on manual teams can erode customer trust and slow response times.

How does AI fit in: By deploying AI chatbots directly within banking websites, mobile apps, messaging platforms, and customer support portals. They are also integrated into ticketing and CRM systems, allowing seamless handoff between automated responses and human agents. AI-powered assistants are managing up to 50% of routine inquiries during peak periods.

Make Sure to Check: These assistants interact with sensitive financial and personal data, so institutions must maintain controls over data access, response accuracy, and escalation processes. Clear governance ensures privacy, compliance, and reliable outcomes.

- Customer Onboarding & KYC Verification

For many Philippine BFSI organizations, manually fragmented onboarding workflows create inefficiencies, compliance gaps, and negative customer experiences.

How does AI fit in: AI is built into digital onboarding workflows within apps and online portals, where it processes customer submissions in real time. It extracts structured data from uploaded documents, validates identity through biometric checks, and cross-references information against internal and external databases.

Make Sure to Check: Human intervention is still essential for flagged cases, complex profiles, and exceptions to ensure compliance with local regulatory expectations. Clear governance, review checkpoints, and auditability ensure that efficiency gains are balanced with accountability and regulatory integrity.

- Fraud and Scam Detection

Risk of fraud and scams increases with mobile banking adoption, while unclear accountability slows response.

How does AI fit in: An AI-supported system can block or delay the transaction, require step-up verification (such as OTP or in-app confirmation), or generate alerts within fraud monitoring and case management systems that’s within core banking systems, payment gateways, mobile banking apps, and online banking platforms, where it evaluates transactions at the point of initiation and before final processing.

Make Sure to Check: AI-powered detection must remain explainable and consistent. Excessive false positives or poorly managed alerts can disrupt legitimate transactions and erode customer trust, making clear governance, review processes, and auditability essential.

Internal-Facing Applications

Beyond customer interactions, AI also drives efficiency and risk management within internal operations.

- Operational Efficiency and Process Automation

The fragmented, manual internal workflows create bottlenecks and inconsistent outcomes.

How does AI fit in: AI is integrated into internal processing systems and workflow tools, where it handles structured, repeatable tasks across departments. It validates and reconciles data between systems, processes documents within operational queues, and routes items based on predefined logic.

Make Sure to Check: Even internal automation affects regulated processes. Outputs require active monitoring and governance to maintain data integrity, audit readiness, and compliance.

- Credit Risk Assessment

The traditional credit evaluation lags real-time customer behavior, causing delays and potential misalignment with risk frameworks.

How does AI fit in: AI is integrated within credit evaluation and loan processing systems, where it continuously analyzes both historical and real-time data inputs. It generates risk scores during application processing, supports decision thresholds for approvals, and flags applications that fall outside defined parameters.

Make Sure to Check: Despite automation, credit risk decisions must remain transparent, explainable, and aligned with regulatory and internal risk frameworks. Human oversight is essential, especially for complex or borderline cases.

- Anti-Money Laundering (AML) and Transaction Monitoring

Rising transaction volumes and increasingly sophisticated financial crime are overwhelming traditional rule-based monitoring systems, generating large numbers of low-value alerts and diverting compliance teams from high-priority investigations.

How does AI fit in: AI is embedded within AML monitoring and case management systems, where it analyzes transaction relationships and behavioral patterns across accounts, prioritizes alerts based on risk scores, and surfaces them within investigation tools used by compliance teams.

Make Sure to Check: AML processes must remain fully traceable and defensible. Leadership is accountable for ensuring AI-driven decisions meet regulatory requirements, are auditable, and can withstand supervisory review. Robust governance, clear escalation protocols, and ongoing model validation maintain regulatory confidence and operational integrity.

These examples highlight not just AI’s value, but also the unique responsibilities and regulatory requirements that Philippine BFSI organizations face.

A Secure AI Adoption Strategic Guide for Philippine BFSI

With the challenges of AI adoption clearly identified, the next priority for Philippine BFSI organizations is securing AI adoption—embedding AI into operations in a way that drives innovation, efficiency, and customer value without creating blind spots.

Secure AI adoption ensures that innovation does not come at the expense of control, accountability, or regulatory compliance. It enables organizations to leverage AI for operational efficiency, enhanced customer experience, and competitive advantage, while keeping risk management, oversight, and regulatory obligations front and center.

This is not just a technology initiative. Secure AI adoption is a strategic approach that combines governance, controls, and accountability with operational execution, ensuring AI becomes a reliable, traceable, and defensible part of everyday workflows.

At its core, secure AI adoption answers three critical questions for BFSI leaders:

- How can AI be applied safely and consistently across the organization?

- Who owns AI-driven decisions and outcomes?

- How can organizations maintain visibility, control, and regulatory compliance as AI scales?

To address these questions, we propose a Five-Pillar Framework — a strategic guide for responsible, scalable AI adoption.

- Accountability & Ownership

AI outputs only become reliable when it’s clear who is responsible for their use and the decisions they influence.

Core Question: Who owns AI risk and decision accountability?

Objective: Establish clear responsibility for how AI is introduced, used, and acted upon across functions.

Action Items:

- Assign AI ownership roles across business, risk, and technology

- Define escalation for AI-related errors or anomalies

- Maintain detailed audit trails of AI-supported decisions

What This Enables:

- Defined ownership of AI-supported decisions

- Clear escalation paths for errors or anomalies

- Traceable, defensible outcomes

- Data Access & Control

Sensitive financial and customer data must be handled carefully as AI systems process and move information in ways traditional controls weren’t designed for.

Core Question: What data can AI access, and under what conditions?

Objective: Define boundaries for AI interaction with sensitive customer and financial data.

Action Items:

- Classify data based on sensitivity and regulatory requirements

- Restrict AI access to only what is necessary for its function

- Implement monitoring and logging of AI data usage

- Ensure encryption and secure processing for all sensitive AI operations

What This Enables:

- Controlled exposure of sensitive information

- Compliance with regulatory and internal data governance standards

- Alignment with operational risk management and privacy obligations

- Standardized AI Usage

Consistent application of AI ensures outcomes are predictable, controllable, and aligned with organizational objectives.

Core Question: How is AI applied consistently across teams?

Objective: Implement organization-wide standards for AI use and approved workflows.

Action Items:

- Develop AI use policies, guidelines, and approved workflows

- Standardized AI model validation, testing, and deployment processes

- Ensure all teams follow the same frameworks for input, output, and monitoring

What This Enables:

- Consistency across business units and processes

- Clear alignment between AI outputs and organizational objectives

- Reduced variability that can lead to compliance or operational gaps

- Human Oversight & Control Points

Even automated decisions in high-impact areas require human judgment to mitigate risk and ensure accountability.

Core Question: Where is human judgment required in AI-supported workflows?

Objective: Define checkpoints where human validation is critical.

Action Items:

- Identify high-impact AI decisions that require human review.

- Establish approval workflows for critical or risk-sensitive outputs.

- Train staff to interpret AI outputs and intervene when necessary.

What This Enables:

- Prevention of over-reliance on AI outputs

- Clear approval paths in high-impact or risk-sensitive processes

- Maintainable, explainable, and defensible decision-making

- Continuous Monitoring & Governance

AI adoption evolves over time, and without ongoing oversight, small gaps can become systemic risks.

Core Question: How is AI usage tracked, reviewed, and improved over time?

Objective: Maintain visibility and control as AI adoption scales across the organization.

Action Items:

- Implement continuous monitoring dashboards for AI performance and compliance.

- Conduct periodic audits of AI models, data usage, and outputs.

- Update AI policies and workflows as regulations, technology, or risks evolve.

- Track incidents and near misses to improve governance.

What This Enables:

- Early detection of gaps or emerging risks

- Ongoing evaluation of AI effectiveness and alignment with business objectives

- Audit-ready documentation for regulatory review

For organizations looking to deepen governance structures, accountability models, and regulatory alignment, explore How Do Financial Organizations Build an Effective AI Governance Framework.

How to Operationalize the Framework

A framework alone is not enough — execution requires tools, platforms, and partners that integrate governance into everyday workflows.

- Modern work platforms, such as Microsoft’s ecosystem, can embed AI securely into operations, enabling visibility, traceability, and collaborative decision-making.

- A trusted partner like Tech One Philippines helps operationalize governance, implement controls, and ensure regulatory compliance—allowing BFSI organizations to scale AI safely without slowing innovation.

By combining strategic governance, structured processes, and the right technology enablers, BFSI organizations can:

- Scale AI adoption confidently across operations

- Protect customer trust and institutional integrity

- Turn AI into a strategic differentiator rather than a risk exposure

Turning Strategy into Action

Secure AI adoption is both a strategy and a capability. The five-pillar framework provides a practical blueprint for embedding accountability, standardizing usage, controlling data, enforcing oversight, and continuously monitoring.

To help BFSI leaders translate this framework into action, we’ve created two complementary resources:

- An infographic that simplifies the five-pillar framework into a clear, easy-to-understand model

- A self-assessment checklist that helps organizations evaluate whether these pillars are in place across their operations

Together, these tools enable organizations to quickly assess AI readiness, identify governance gaps, and prioritize next steps—without wading through pages of text.

Enabling Secure AI Adoption with Tech One Philippines

Secure AI adoption requires more than strategy—it demands operational alignment, technological expertise, and trusted partners. Tech One Philippines helps BFSI leaders turn secure AI strategies into actionable execution by integrating governance, platform controls, and employee adoption, ensuring AI can be safely embedded across everyday workflows. With deep experience in Philippine BFSI environments, Tech One guides organizations through regulatory expectations, operational constraints, and risk management, enabling scalable, compliant, and traceable AI adoption while preserving visibility, accountability, and customer trust.

Recognized as Microsoft’s Country Partner of the Year 2025, Tech One Philippines brings proven expertise in deploying Modern Work and AI solutions within regulated environments. By aligning strategy with technology and operational execution, BFSI organizations can innovate confidently without compromising compliance or oversight.

Plan your next steps today with our Secure AI Readiness Assessment to evaluate your organization’s AI governance, controls, and operational preparedness!